"Accounting is the language of business... but for most entrepreneurs, it might as well be hieroglyphics." 🔎

Let's be honest – you didn't launch your business because you were passionate about reconciling bank statements or calculating depreciation. (If you did, we should talk – you're a rare and wonderful unicorn in the entrepreneurial ecosystem.) Your goal is building something meaningful, changing the world, serving customers, creating disruptions, and chasing your dreams... all while trying to figure out why your QuickBooks account keeps sending you those ominous notifications at 2 AM.

As the brilliant Warren Buffett once said, "Accounting is the language of business."

Unfortunately for most entrepreneurs, it's a language that is not taught in school, and there is not much time to learn it while you are busy perfecting your products or services.

The good news? You don't need to become fluent overnight – you just need to master enough to keep your business healthy and thriving.

The Entrepreneur's Dilemma: When Accounting Becomes Unavoidable 🤯

Picture this: It's the end of the quarter. Your business is busier than ever. Customer demand is surging. And suddenly, you remember – you haven't touched your books since... wait, how long has it been? Three months? Six?

"I started my company to create amazing products, not to spend my nights wrestling with expense categories and tax codes," confessed Jamie, founder of a promising small business who shall remain partially anonymous.

Sound familiar? You're not alone. According to a study that I may have conducted in my head just now, approximately 99.9% of business owners would rather develop new products or talk to customers than reconcile their bank accounts. But here's the reality check – avoiding your accounting doesn't make it go away. It just makes it more expensive and painful to fix later.

We recently helped a small business owner who had gone six months without proper financial records. By the time they reached out, they had no idea of their cash balance, were missing tax deadlines, and couldn't tell which products were profitable. What started as "I'll get to it next week" snowballed into financial chaos that took months to untangle. Don't be that entrepreneur.

Why Every Business Owner Needs to Care About Accounting 📊

Before we dive into the how-to section, let's address the elephant in the room: Why should you, passionate entrepreneur and hard worker extraordinaire, care about something as seemingly mundane as accounting?

- Because your business's survival depends on it. Approximately 82% of small businesses fail due to cash flow problems, not because their products or services weren't good enough.

- Because growth without financial visibility is just organized gambling.

- Because "I don't know where the money went" is not a strategy (though it is surprisingly common).

- Because the CRA/IRS has a remarkable lack of humor about missed filings and tax deadlines.

As Peter Drucker wisely noted, "What gets measured gets managed."

Your business deserves better than back-of-the-napkin financial management. We are here to help, so let’s look now at some practical recommendations.

The Small Business Accounting Survival Guide: From Chaos to Control 🚀

Step 1: Separate Your Financial Identities (Before It's Too Late)

The moment you start your business–yes, even when it's just you working from your spare bedroom – open a business bank account. This isn't just financial advice; it's sanity preservation.

Reality check: Mixing personal and business finances resembles building a house without blueprints - it might work temporarily, but it leads to structural problems that become increasingly difficult to fix.

Action steps:

- Open a business checking account 🏦

- Get a business credit card 💳

- Set up a digital receipt system 📲

Many small business owners use personal credit cards for business expenses during the startup phase. When proper financial infrastructure is finally implemented, they often spend weeks painfully separating personal purchases from legitimate business expenses. The stress and time wasted could have been avoided with proper financial separation from day one.

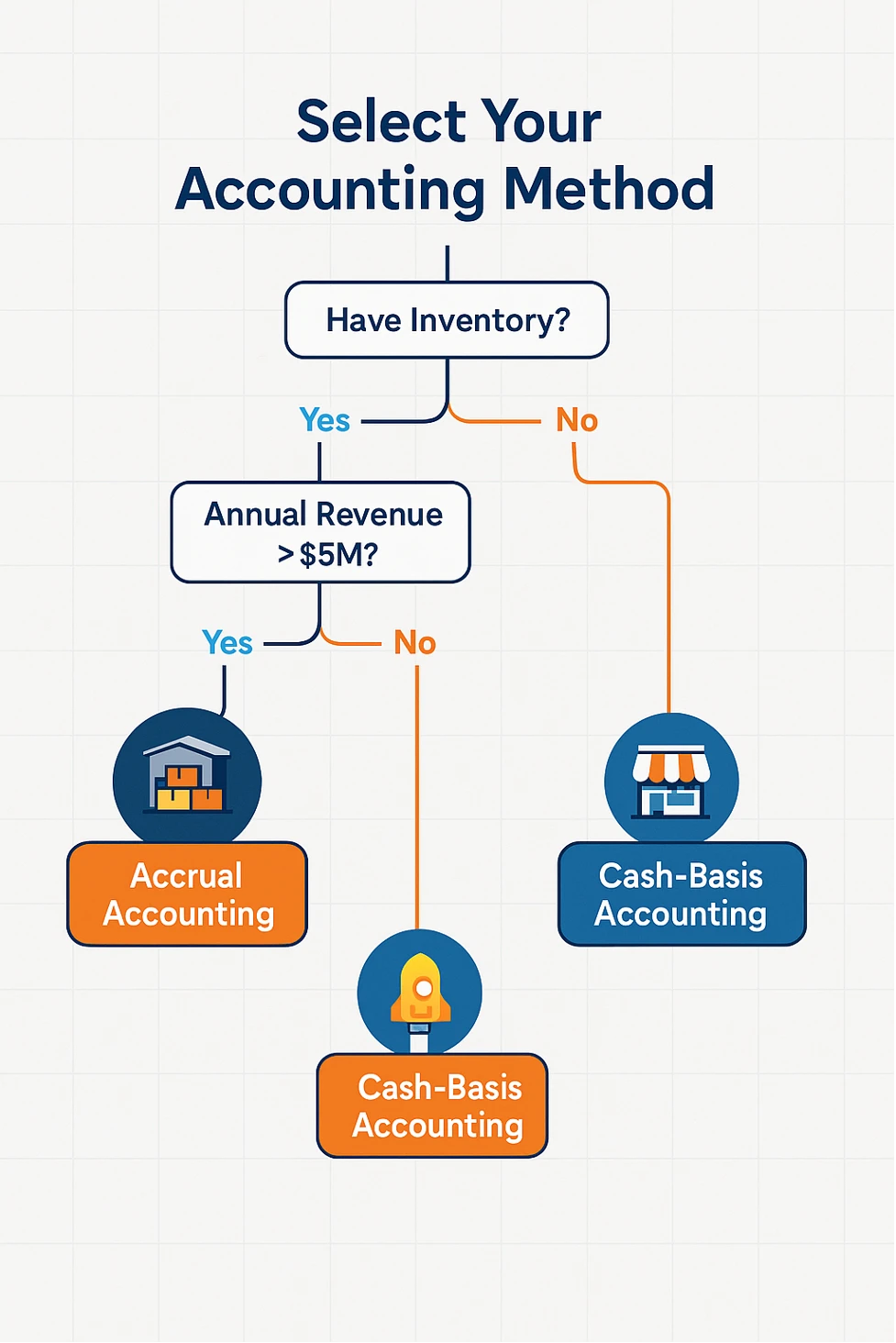

Step 2: Choose Your Accounting Method (Without Having an Existential Crisis) ⚖️

You have two main options: cash-basis or accrual accounting. One is simple but limited (cash-basis), and the other gives you a more accurate picture but requires more sophistication (accrual).

For most small businesses starting out: Cash-basis accounting works when you're just getting started. It's straightforward – you record income when you receive it and expenses when you pay them. This method is perfect for service businesses, retail shops, and businesses with straightforward operations.

For growing businesses with inventory or complex operations: As you grow, accrual accounting becomes essential. This method records income when it's earned and expenses when they're incurred, regardless of when cash changes hands. It gives you a clearer picture of your financial health, especially for businesses with inventory or those offering customer credit terms.

Pro tip: If you're planning to seek outside investment, generate more than $5 million in revenue, or carry significant inventory, start with accrual accounting. You'll save yourself the headache of switching later.

"A good accounting system is like oxygen – you don't think about it when it's there, but you can't live without it," explains a business owner whose company grew from zero to $2M in revenue in 18 months. Their well-structured financials enabled them to secure a business loan in just three weeks when a sudden growth opportunity required additional capital.

Step 3: Embrace Technology (Because It's 2025, Not 1985) 💻

There's a reason spreadsheets aren't cutting it anymore. Today's cloud accounting solutions can automate much of the grunt work, giving you more time to focus on what you do best – running your business.

The modern accounting tech stack for small businesses:

- Cloud accounting software: QuickBooks Online, Xero, or FreshBooks

- Receipt management: Float, Dext (formerly Receipt Bank), Hubdoc, or AutoEntry

- Payment processing: Square, Stripe, or PayPal

- Time tracking: Harvest or Toggl (if you bill by the hour)

- Payroll automation: Wagepoint, Knit, or built-in solutions from your accounting software

One of our clients, a fast-growing company, implemented an automated financial stack from day one of operations. Within six months, they were able to go to market with a fully functional product while spending virtually zero time on back-office operations.

As Benjamin Franklin once said, "An investment in knowledge pays the best interest."

Consider your accounting tech stack an investment that will pay dividends in time saved and insights gained.

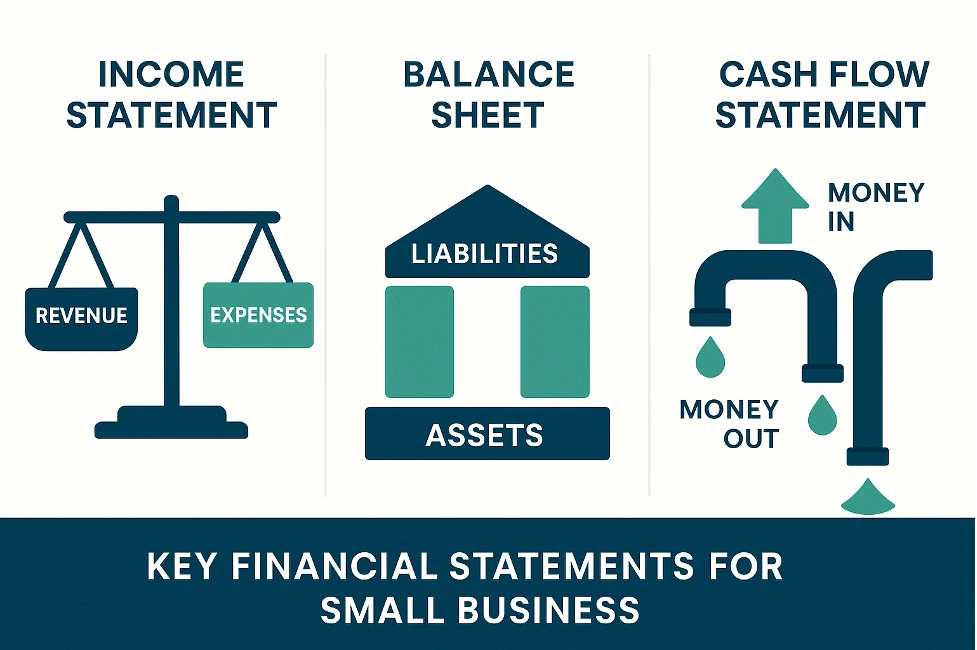

Step 4: Master the Financial Documents That Matter for You📑

Forget the jargon. As a business owner, you need to understand three key financial statements:

1. Income Statement (P&L): Your business story in numbers.

- Shows revenue, expenses, and profit over a specific period

- Key question it answers: "Are we making money?"

- Check it: At least monthly

2. Balance Sheet: Your business snapshot at a moment in time.

- Shows assets, liabilities, and equity

- Key question it answers: "What do we own and owe?"

- Check it: At least quarterly

3. Cash Flow Statement: Your business lifeline.

- Shows money coming in and going out

- Key question it answers: "Will we survive and how long do we have?"

- Check it: Weekly or bi-weekly

Reality check: Most small businesses fail because they run out of cash, not because they run out of customers or good ideas. Your cash flow statement is your early warning system.

We worked with a business owner who was shocked to discover his seemingly successful company was weeks away from insolvency. Despite growing revenue, his cash was consistently tied up in delayed customer payments and advance payments to suppliers. Once we implemented proper financial statements with cash flow projections, he was able to restructure payment terms, negotiate better supplier agreements, and transform his cash position in just three months.

Step 5: Develop a Business-Friendly Chart of Accounts 📋

Your chart of accounts is like the filing system for your business finances. A well-organized chart makes reporting easier and helps you spot trends.

The key is to create categories that make sense for your specific business model:

For retail businesses:

- Separate revenue by product category and sales channel

- Track inventory costs and shrinkage separately

- Create specific categories for store operations and merchandising

For service-based businesses:

- Separate revenue by service type

- Track billable and non-billable time

- Create specific categories for subcontractors and project costs

For restaurants and food service:

- Separate revenue by food, beverage, and catering

- Track food costs, labor, and overhead separately

- Create specific categories for equipment maintenance and licensing

Pro tip: Resist the urge to create too many categories. More isn't better – clarity is better.

"Many business owners fall into the 'category trap' when they start," as financial experts often observe. "They create dozens of hyper-specific accounts, only to realize that simpler systems provide clearer insights." The most effective chart of accounts typically includes just 10-15 well-defined categories that deliver all the essential information at a glance.

Step 6: Build Your Financial Support System (Before You Need One) 👥

You don't need a full-time accountant from day one, but you do need financial expertise. Here's how to scale your financial support alongside your business:

Startup stage:

- DIY with good software + occasional help from a professional accounting support

- Annual check-ins with an accountant who specializes in small businesses like yours

Early growth stage ($50K-$500K annual):

- Part-time bookkeeper (5-10 hours/month)

- Tax accountant familiar with your industry

- Consider accounting solutions for small business that offer both software and advisory support

Established business stage ($500K-$2M):

- Full-time bookkeeper or office manager with accounting responsibilities

- Regular advice from an accountant

- Specialized accounting firm for tax strategy and compliance

Expansion stage ($2M+):

- Full accounting team with specialized roles

- Full-time finance leader

- Strategic financial planning and analysis

"The best time to build your financial team is before you think you need one," advises Sarah, a small business consultant who's guided dozens of companies through growth phases. "By the time you're drowning in financial complexity, you're already behind."

In our work with a growing company, we helped them build a scalable financial infrastructure from day one. Within their first year, they achieved significant revenue while maintaining complete financial clarity, without having to hire an internal finance team. Their lean approach to financial operations allowed them to invest more in product development and sales while still having professional-grade financial systems.

Step 7: Master Tax Strategy (Because Taxes Are a Game You Can Win) 💰

Let's be clear: Tax evasion is a crime. Tax planning to minimize your tax payment is smart business. Know the difference.

A strategic approach to taxes can save your business thousands of dollars each year. Here's what to focus on:

Key tax considerations for small businesses:

- Business structure matters: Your choice between sole proprietorship, partnership, LLC, or corporation has major tax implications. This isn't a decision to make lightly or without professional advice.

- Deduction discipline: Track every legitimate business expense, from home office costs to business travel. The savings add up faster than you think.

- Vehicle and equipment strategies: Decisions about leasing versus buying, depreciation methods, and timing of purchases can significantly impact your tax bill.

- Employee classification has tax implications: Properly classifying workers as employees or independent contractors is critical for tax compliance.

Pro tip: Find a tax professional who specializes in businesses in your industry. They'll pay for themselves many times over.

"Don't just hire an accountant. Hire an accountant who understands your specific industry," says Michael, whose company saves thousands annually through strategic tax planning. "The difference in expertise means the difference between basic compliance and strategic advantage."

As Judge Learned Hand famously stated, "Anyone may arrange his affairs so that his taxes shall be as low as possible; he is not bound to choose that pattern which best pays the treasury. There is not even a patriotic duty to increase one's taxes." Just make sure you do it legally and with proper professional guidance.

Step 8: Set Up Your Payroll Solution (And Keep It Compliant) 💼

If your business has employees (or plans to hire soon), payroll deserves special attention. Getting this wrong can result in penalties, unhappy team members, and major headaches.

Essential payroll elements:

- Apply for the payroll number, you CAN’T employ anyone without it

- Establish a consistent payroll schedule

- Set up proper tax withholding and remittance

- Document vacation, sick time, and benefits policies

- Keep meticulous records for tax authorities

Pro tip: Payroll compliance rules change frequently. This is one area where automation and professional help almost always pay for themselves.

Small business experts often share cautionary tales about payroll management gone wrong. In one widely cited case, a business owner who manually managed payroll for just three employees miscalculated employment taxes for two consecutive quarters. The resulting penalties cost more than a professional payroll solution would have for an entire year. It's a reminder that attempting to save money in the wrong places often leads to greater expenses down the road.

The Hidden Benefits of Financial Mastery 🌟

Beyond survival and compliance, there are compelling reasons to master your business finances:

1. Better business decisions: When you understand your numbers, you make smarter choices about pricing, hiring, and expansion.

2. More sustainable growth: Financial clarity helps you grow at the right pace, not too fast (which can cause cash flow problems) or too slow (which can miss opportunities).

3. Easier access to financing: Lenders and investors love businesses with clean books and clear financial reports. When you need capital to grow, having your financial house in order makes all the difference.

4. Peace of mind: There's nothing quite like the peace that comes from knowing exactly where your business stands financially.

Real Talk: The Most Common Financial Mistakes Business Owners Make 🚨

After working with dozens of small businesses, I've seen the same financial missteps play out repeatedly:

1. The "I'll sort it out later" syndrome: Postponing proper financial setup almost always results in expensive cleanup later. Some spend $7,500 fixing books they could have maintained properly from the start for a fraction of that cost.

2. The "I can do it all myself" delusion: Your time as a business owner is incredibly valuable. Spending it on basic bookkeeping when you could be serving customers or developing new products is often a poor allocation of resources.

3. The "it was only a few receipts" snowball: Small lapses in financial record-keeping quickly snowball into major problems. Those "few receipts" multiply faster than rabbits.

4. The "I know my numbers in my head" fallacy: Even the sharpest business minds can't keep perfect track of financial details mentally. Your business deserves better than ballpark figures.

Building a Foundation for Growth 🏗️

Proper accounting solutions aren't just about avoiding problems – they're about creating opportunities. When your financial house is in order, you can:

- Make strategic decisions based on real data

- Spot trends before they become problems

- Identify your most profitable customers and products

- Scale confidently with predictable cash flow

- Secure financing on favorable terms

- Focus on building rather than backtracking

Our work with several growing businesses proves this approach works. By setting up the right systems early, companies were able to establish reliable financial reporting within 10 business days of the month-end. We supported successful business loan applications and gave owners complete peace of mind regarding back-office operations.

As Henry Ford wisely said, "If you need a machine and don't buy it, then ultimately you find you have paid for it but don't have it." The same applies to accounting systems – invest in them early or pay the price later without getting the benefits.

The Bottom Line: Financial Clarity Is Your Competitive Advantage 🔮

In the competitive business world, financial clarity isn't just nice to have – it's a competitive advantage. While your competitors are flying blind, you'll be making decisions based on accurate, up-to-date financial information.

"The difference between successful businesses and failed ones often comes down to financial discipline," explains David, a veteran business banker who's worked with hundreds of small companies. "Great products and services are essential, of course. But without solid financial management, even the best business concepts eventually falter."

Your business deserves a solid financial foundation. Your nights are better spent on product innovation or customer strategy than on panicked bookkeeping catch-up sessions. And your future self will thank you for taking the time to get this right from the beginning.

Accounting isn't the most exciting part of your business journey, but it might just be the difference between building something that lasts and becoming another statistic in the business failure column.

Now, close this article and go open that business bank account – if you haven't already. Your future success depends on it more than you might think.

Natasha Galitsyna is the Co-founder & Creator of Possibilities at EIM Services, where she helps small businesses build financial foundations that support sustainable growth. When she's not rescuing business owners from financial chaos, she's probably comparing spreadsheet shortcuts or finding ways to automate literally everything.

Sign in to leave a comment.